Income from short-stay accommodation activity must be reported in full, even if the property has multiple owners. The profit/loss (calculated as income minus expenses) is divided among the owners. If a profit is made, each individual’s tax is based on their share of the profit and their personal tax rate.

Example A:

Jill and Bill jointly own a second property in Nelson, which they rent out on Bookabach year-round. The short-stay accommodation generates an annual income of $50,000, with total expenses of $32,000. This leaves a taxable profit of $18,000. Since the property is jointly owned, the profit is split equally—$9,000 each. Jill and Bill then pay tax on their respective $9,000 shares at their individual tax rates.

Example B:

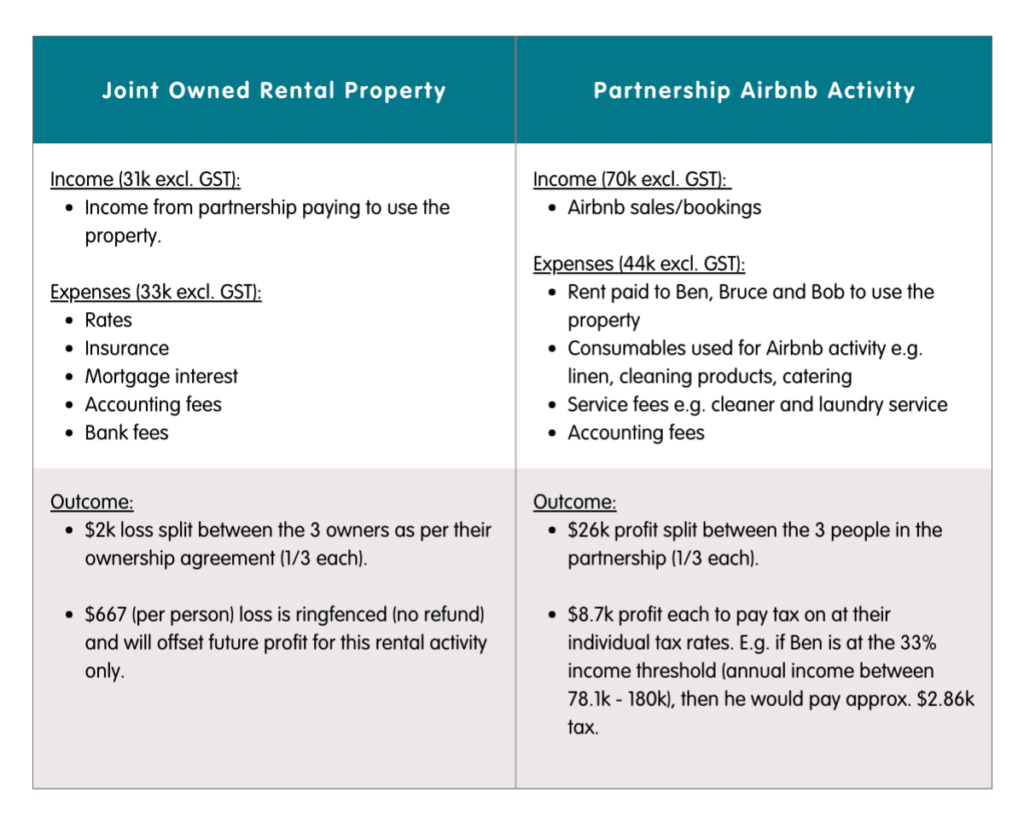

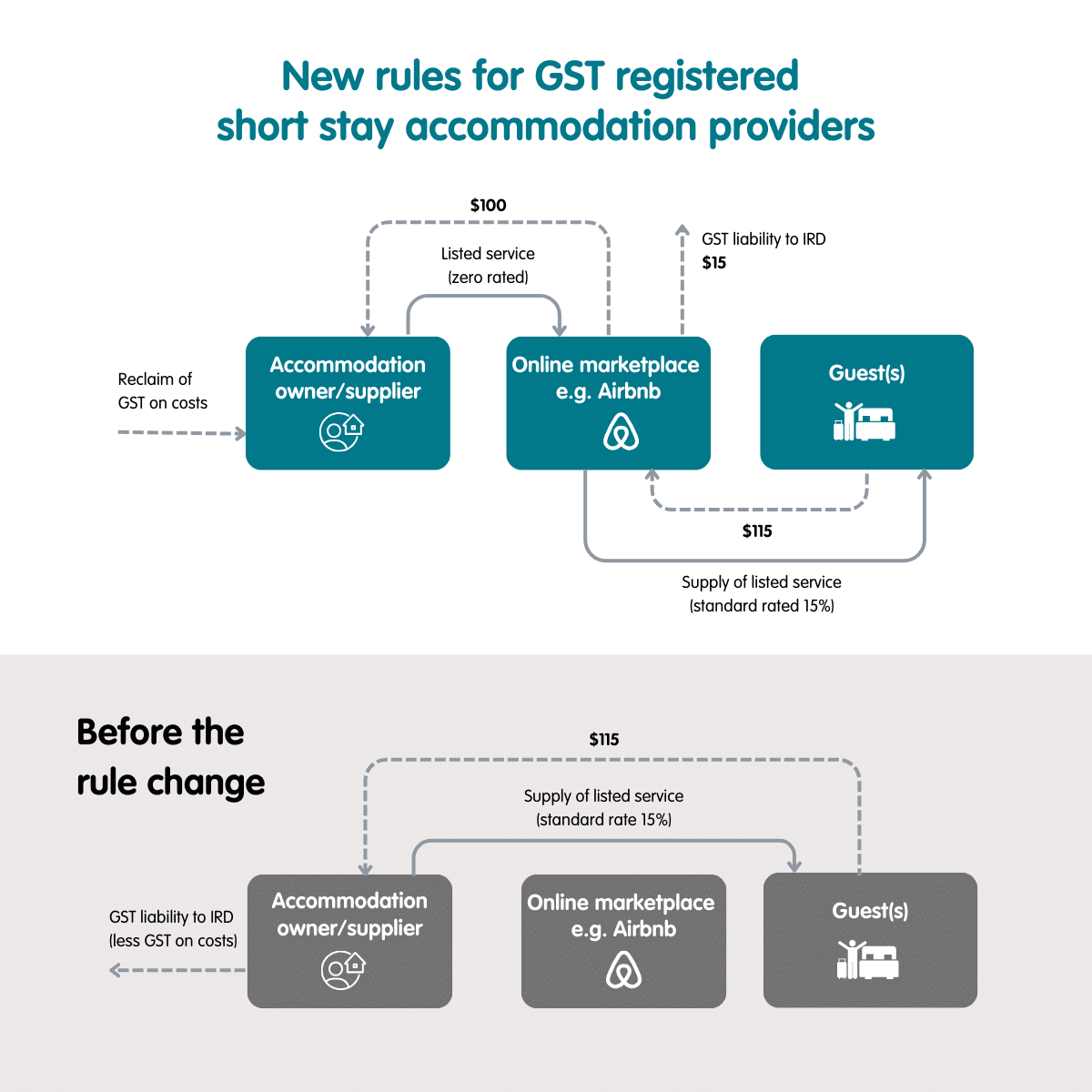

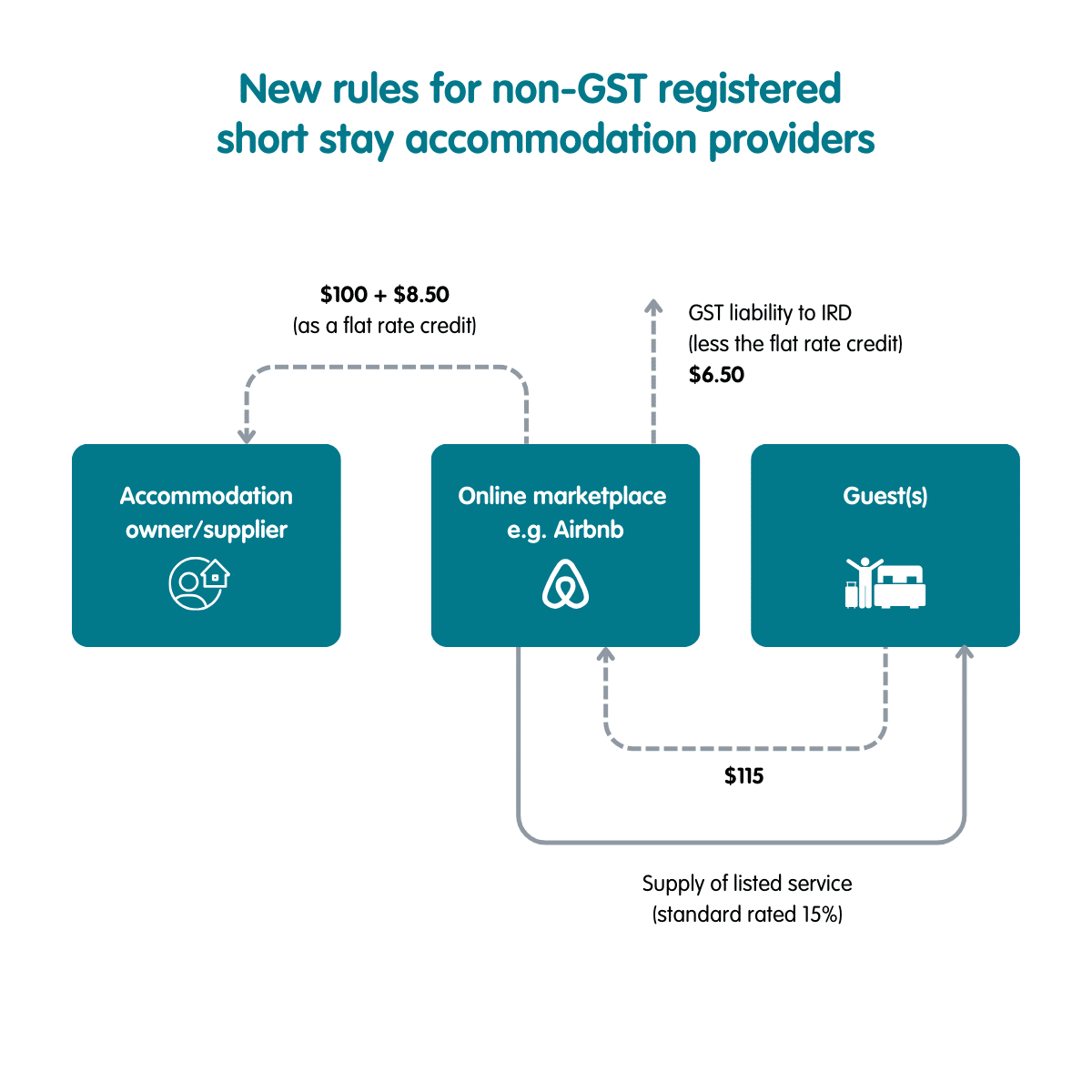

Bob, Ben and Bruce jointly own a property in Christchurch with two dwellings, purchased in 2016. Bob, Ben and Bruce live in the dwelling in the front of the property and they rent out the separate dwelling at the back of the property year round on Airbnb. The rear dwelling brings in an annual income of $70,000 (excl. GST), which requires them to register for GST. Since they can’t be GST registered as joint owners for this activity, their accountant advised them to set up a partnership/company and register for GST. Bob, Ben and Bruce decided a partnership would be the best fit for them.

Bob, Ben and Bruce have a tenants in common agreement stating they own equal thirds in the property. Now that the rental activity maybe say Airbnb activity rather than “rental” will be run through the partnership, the joint owners Bob, Ben and Bruce will be ‘leasing’ the property to the partnership to use to generate short-term accommodation income.

Each year Bob, Ben and Bruce’s accountant will complete two sets of accounts.